(Amended)

Introduction

Delegates, here is the amended September MERC Newsletter, first version sent on 2nd Oct, this version has adjusted commentary to Resources for Regions section to ensure clarity with the program, put accommodation options – Blayney meetings on 27th November & comments on the upcoming Executive Committee elections for delegates that may be attending remotely.

Please circulate the Newsletter to your fellow Councillors and senior staff, so they can appreciate and understand the excellent work the Association and you are doing on behalf of your Council and community, with regard to mining and energy related matters.

COVID-19 Virus Impact on MERC

The NSW Government is working very closely with Councils to support communities across the state in response to COVID-19. Consequently, there will be changes as circumstances alter that will affect MERC and members going forward due to the NSW Government’s respective Ministerial Public Health Orders to implement controls as necessary to combat the COVID -19 Virus.

The next MERC Ordinary meeting will be held on 27th November 2020 as a “face to face” meeting at Blayney with capability to attend by video conference and the Executive Committee having a zoom meeting on 20th November 2020, in view of the Covid-19 position.

Two year terms and Nominations for Executive Committee

MERC is to consider the Executive Committee being elected for two year terms and to clarify the wording in Clause 7.1 of the constitution on the composition of the Executive Committee on whether two from any one member Council can be on it, at a future Special General meeting of MERC.

Executive Committee currently comprises Chair, two Deputy Chairs and three other delegates with all to come from separate council areas and they are elected annually, however recent events have demonstrated the clause needs rewriting for clarity purposes.

At the Executive Committee meeting on 14th August 2020, it was agreed that the interpretation will be as follows until the Constitution wording is improved.

“it is understood that the position has always been that representation from as many separate members as possible be on the Executive Committee, unless there are not enough nominations, then multiple representation can occur”.

Next Meetings for the Association in 2020

The remaining meetings in 2020 were agreed to be held by zoom for the Executive Committee on 20th November 2020 and the Ordinary, AGM & Special Meeting to be held at Blayney on 27th November as a “face to face “ meeting with video conferencing options.

Accommodation in Blayney – Blayney Central Motel ph 02 63683355; Blayney Goldfields Motel ph 02 63682000; Blayney Budget Leumeah Motel ph 02 63682755; Blayney Caravan Park ph 02 63632799; Royal Hotel ph 02 63682210 and Exchange Hotel 02 63682124.

Meetings and Executive Committee Elections

Under the constitution, MERC is required to have one General Meeting (the Annual General) a year and as many other General (Ordinary) Meetings as the Executive Committee determine. MERC must have four Executive Committee meetings a year. The Executive is to be elected annually at the AGM by delegates.

Note that in the MERC constitution there is no postal voting (Clause 14.3) or provison for those attending the meeting by video or tele-conference on how to vote, even though if requested, tele-conferencing facilities are to be made available (Clause 4.4). What does this mean are delegates regarded as present if on video or phone and how do they vote remotely, in this present day and age since Covid? Executive Officer is to investigate the options, interpretations with Dept Fair Trading and other Associations that have addressed this.

Elections are conducted as per Clauses 14.6.and 14.7 taking into account the Voting Methods used in Annexure A to the Constitution for Chair, Deputy Chairs & Executive Committee – by ordinary ballot, open voting and/or preferential. These voting methods will require the voter to be present when election is held, unless the platform that the video/tele conferencing is on can conduct the voting process electronically and legally otherwise the hard line interpretation is that the voter must be present at the meeting to vote.

If any any changes are required to the constitution they must be made at a General (Annual or Special) Meeting with at least two thirds of the delegates present at the meeting to agree to such alterations or amendments. More later once situation is clarified

Update on the Voluntary Planning Agreement

The Guidelines for VPA’s and a VPA framework agreement (including scope and calculation methodologies) has been agreed to by NSWMC & the MERC VPA Working Party and DPIE have put on their website. The link is:

Resources for Regions (R4R).

Details were recently released on Round 7 of the Resources for Regions Program as announced by the Deputy Premier, Hon John Barilaro, which was very well received by members, particularly the 24 eligible LGA’s.

At the meeting on 14th August 2020 the Executive Committee on behalf of all members, requested the Executive Officer seek clarification on the program criteria as initially displayed to the working party there were 31 LGA’s listed, however the final list was 24 and it wasn’t clear the reasons for the reduction.

The Executive Officer had discussions with DPIE, Regional NSW Department, Executive Director Regional Programs, Johnathon Wheaton and his team recently and he provided the following clarification, which is repeated as important information to note for members:

” Good to catch up with you today. As outlined on the Program website, several factors were considered in determining eligible LGAs for Round 7 of Resources for Regions. These included:

- the LGA mining employment Location Quotient (LQ)

- number of active mines in the LGA

- level of mining activity in the LGA

- funding previously received under the Resources for Regions program.

The employment Location Quotients (LQ) is based on place of employment in the ABS Census Place of Work data and is used as an indicator of the relative importance of, or reliance on, an industry or sector in an LGA or region compared with a reference economy. For the purposes of the Resources for Regions program, the whole of NSW is the reference economy (represented by an LQ of 1.0). As an indication, higher LGAs have an LQ over 40. For the examples you gave:

- MidCoast LGA has a mining employment LQ of 0.90; mining activity is relatively low compared with other LGAs; and MidCoast LGA has not received funding under the previous six rounds of the Resources for Regions program.

- Forbes Shire LGA has a mining employment LQ of 0.31; mining activity is relatively low compared with other LGAs; and Forbes LGA has not received funding under the previous six rounds of the Resources for Regions program.

Both Forbes Shire and MidCoast LGAs are eligible for all other Regional Growth Fund programs, receiving over $10 million (15 projects) and $17 million (62 projects) respectively so far.

It is standard practice that the Department will review mining data and other information prior to any future round of the Resources for Regions Program to consider any significant changes in the level and potential impact of mining in an LGA. We balance high transparency with strong probity and processes across all our programs – Resources for Regions is no different. There is a vast amount of information about the Program on the Resources for Regions webpage, and an especially long list of FaQs.

Membership Campaign

At the Ordinary meeting in Sydney on 5th March 2020, it was agreed that MERC authorise the Executive Officer to develop and implement a marketing campaign in consultation with the Chair and relevant MERC membership staff to include pamphlets, notepads with “We are your voice – become a member” or suchlike on them for handouts, a banner indicating locality of members throughout NSW, a video to play on a laptop to link back to the webpage, set up a membership page on the website, etc to the value of $5000 plus take a stand at the LGNSW Conference in November 22-24, at Cessnock and do a presentation to the Country Mayor’s Association at a future meeting.

Unfortunately, due to COVID 19, whilst a stand was booked for the LGNSW, this has been cancelled in its usual format and will now be a half day virtual conference, which doesn’t suit an organisation like ours, relying on “face to face” conversation and relationship selling.

Discussions on the content of a membership web page and the marketing content with the principal of Cibis has occurred. Volunteers to provide testimonials via video have been sourced by the Executive Officer who is now in pursuit of them and has provided scripts and guidleines for their videos.

Chair and Executive Officer presented the merits of MERC membership to Mid Coast Council workshop on 30th September 2020, with feedback that it was very positive.

List of Speakers for future meetings of MERC

MERC will be continually pursuing the following speakers for future meetings with The Greens now listed:

- Hon Rob Stokes, Minister for Planning & Public Spaces, Liberal Party;

- Hon Matt Kean, Minister for Energy & Environment, Liberal Party;

- Hon John Barilaro, Deputy Premier, Minister for Regional NSW, Investment & Trade, Leader of NSW National Party;

- Hon Adam Marshall, Minister for Agriculture & Western NSW, National Party;

- David Shoebridge MLC (Energy) & Abigail Boyd MLC (Mining), from The Greens;

- Other relevant Opposition party members and government senior officers will also be pursued for meetings as required depending on locality of the meetings – Shadow Minister for Local Government (Greg Warren) keen to address delegates post COVID;

- Relevant Senior Departmental Executives;

- CEO’s, Clean Energy Council and Clean Energy Finance Corporation, ARENA, etc.

Speakers organised to date for the November meeting are:

- Dr Alex King, Executive Director, Resources Policy, Planning & Programs to speak on “Strategic Statement on Coal Exploration and Mining in NSW”.

(Will be pursuing relevant local politicians for November meeting eg Donato, Toole)

Research Fellowship Update

Here is the latest update from Peter Dupen (PhD student) which the Executive Officer has followed up as the Executive Committee is keen to see this project commence, recognising the difficulties experienced dureing COVID 19:

“We have reached high-level agreement to work with Aurelia Metals Ltd to enhance their socio-environmental impact scoping process with a set of participatory-modelling (PM)-enhanced stakeholder engagement workshops to gather community and regulatory views on a proposed new metalliferous mine near Cobar, NSW. We are in discussions with Aurelia to confirm an agreement, timings and roles between the academic team, sponsors and their consultants. If all goes according to plan, the engagement would commence in late October.

We have begun designing a web-interface to support this process. This platform will perform a number of functions, including (a) as a repository for public information on the proposal, (b) a host for PM tools when these are developed, (c) a repository for surveys which will be deployed before, during and after the engagement and (d) the host for an algorithm-enhanced discussion forum which will gather views from participants and the broader community on the mine proposal and the engagement process.

The Project Evaluation Plan for the project has been substantially completed (currently under final review) and will be submitted this week to an academic board and to an ethics committee for consideration prior to wider dissemination to sponsors and other interested stakeholders.

The hurdle that has arisen is that UTS will not support the proposed sponsorship agreement on the basis that it requires approximately 35% of the total sponsorship funds ($24.5K from $70K) to be paid to them as university overheads.”

This reaction from UTS was not unexpected, as delegates have previously stated an unwillingness to divert critical project resources to pay university overheads but are still keen for the project to proceed. The Executive Officer has discussed the project status and options with the Chair and will be taking the options to the Executive Committee for a decision shortly for the project to proceed or not. The UTS would continue to be involved as the project remains central to the PhD project for Peter Dupen and MERC and related sponsors.

Strategic Plan 2020 – 2023 Review

The draft Strategic Plan 2020-23 Strategic Directions, Deliverables and Actions compiled by the working party of Cr McRae, Cr Banasik and Glenn Wilcox have been adopted by the Executive Committee to include in the draft Strategic Plan for referral to delegates for their consideration and adoption on 27th November 2020. Any photos of females in mining activities are welcomed to ensure our Strategic Plan is more inclusive. Enquiries to the Executive Officer.

Update on CRC for Transformations in Mining Economies

MERC was invited last year to be a NSW partner in the establishment of the national Cooperative Research Centre (CRC) for Transformations in Mining Economies (CRC TiME) being established in Perth, Western Australia, at University of Western Australia, at no cost to MERC. This fits in with our strategic plan by being involved in making a difference through research partnerships with Universities and industry in Australia on various topics such as rehabilitation and post mining impacts on economies.

The national partnership was required to get the grant to set up the CRC for transforming mining economies from mining to no mining plus value add them. More will come from this partnership and delegates will be kept informed in due course from their regular newsletters.

For instance, MERC has recently received this email from Professor Fiona Haslam-McKenzie, Program Director:

“We are finalising the project submissions for the Co-operative Research Centre for Transformation in Mining Economies Foundational projects, one of which is being led by Dr Renee Young from Curtin University, (Cumulative Impacts and Baselining Regions) and another, Post Mining Land Uses, lead by Professor Andrew Beer from the University of South Australia, which were indicated by you as projects of interest. I am confirming here that you are indeed keen to maintain interest in these projects and to that end, that we might include you as a member of the end-user project committees.

We are finalising what that means in time and we calculate for the entire year, this would work out to be about 1 day a month across the year for each project. We envisage that this would likely be the following sort of activities:

- Participation in end user meetings (likely to be teleconference format) as the project hits milestones;

- Potential organisation of community-based meetings, especially if we plan to have local case studies;

- Possible links to local networks;

- Dissemination of project results.

Would you mind confirming that you are still keen to be a part of this project and that approximately one day a month is an acceptable time commitment?”

The Executive Officer has confirmed an interest in participating in order for MERC to stay in the loop to see what opportunities may emerge for MERC and members in accordance with our Strategic Plan deliverables with research.

Renewable Energy Zones

The NSW Government is implementing three pilots and one of them is the 3,000 megawatt Renewable Energy Zone (REZ) in the Central-West of NSW as part of their Electricity Strategy, Net Zero Plan and the Commonwealth-NSW Memorandum of Understanding on Energy and Emissions. Stu Hodgson addressed delegates on the REZ at the Executive Committee meeting on 14th August 2020 and indicated that they would like MERC to have a representative on their Regional Reference Group going forward, more details to come.

For more information about NSW REZs please visit www.energy.nsw.gov.au/renewable-energy-zones, or email the team at rez@planning.nsw.gov.au.

Submission to the Productivity Commission on its Review of the Infrastructure Contributions System in NSW and their Rating Review

The MERC submission to the Productivity Commission has been submitted to meet the 28th August 2020 extension. This is an extra submission building on the response to DPIE on EPA Act Contributions system by MERC who were asked by the Productivity Commissioner, Peter Achterstraat to make a submission. A copy of the submission has been forwarded to delegates & put on the webpage.

The submission also includes comments on the Productivity Commissions recommendations that mining rating income being reduced to meet the average business rate levy income (which the State Government has supported), if introduced in legislation will be catastrophic for mining councils and needs to be followed up. Bland Shire Council supported by Parkes Shire Council (MERC members) are taking the matter to the LGNSW Conference and their motion has been distributed for members consideration and support.

The Productivity Commissioner has now asked to speak further to MERC representatives on our submission particularly mining planning agreements and is considering options on how this may be done with Covid 19 in conjunction with the Executive Officer. Discussions have been held with the Chair who suggested Warwick Giblin, Oz Environmental, as author of the submission, the VPA Working party (Cr Owen Hasler, Steve Loane, Chair MERC and Executive Officer meeting via video conference. Numbers are limited in view of the nature of the meeting. This is indeed a feather in the cap of MERC & demonstrates our advocay value!

Related Matters of Interest – Mining and Energy Issues

“Enough New Wind and Solar Locked in to Kill Three Coal Generators by 2025” David Leitch writes in Renewal Energy 30th September 2020:

“There is enough new wind and solar capacity locked in to take Australia to a share of about 42 per cent renewables by the end of 2025, and that might be enough to spell the end of the road for up to three incumbent coal generators.

The capacity of new utility-scale supply of wind and solar projects is about 7.3GW. This consists of the uncommissioned part of currently commissioning capacity, projects under construction, a couple of projects that have reached financial close, and some big projects that have announced PPAs with, say, the Queensland government, but have not yet got to financial close.

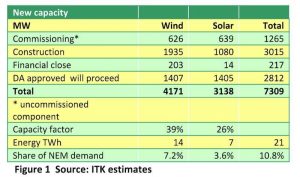

ITK estimates that there is a total of 4.2GW of wind and 3.1GW of solar in those combined categories.

The expected energy from those projects is about 21 terawatt hours, or about 10 per cent of current demand on the National Electricity Market. That’s greater than the combined output of say Yallourn (9.4TWh) and Vales Point B (7.4TWh) but the pain will be spread across generators of every class and every state.

Behind the meter adds another 10TWh by 2025.

But wait, there’s more! Even assuming behind the meter slows down to, say, an average capacity add of 1.5GW per year over the next 5 years, that’s still a cumulative 7.5GW of new rooftop solar capacity, delivering about 10TWh a year at a 15% capacity factor. This will more than offset the anticipated business-as-usual demand growth of 3TWh.

Of course, demand might grow more if the numbskull federal government would incentivise electric vehicles as any security conscious government would already have started to do now there is an alternative technology. However, I hold no great hopes on that score and ITK forecasts total demand growth of 0.5% per year.

This could force three coal generators to close within 5 years, but the pain will be spread out.

So in total we anticipate that even without the addition of more announced winding solar projects between today and the end of 2025, thermal generation output will nevertheless decline by about 26TWh (from 145TWh in 2020 to 119TWh in 2025).

That’s enough to close three coal generators, eg Vales Point, Yallourn and one in Queensland, say parts of Tarong. However, gas generation might lose some of the little market share it has left and the other coal generators might all cede market share as an oligopoly and try to keep prices up. There is a lot more to be said on this but in this note we only get to the headlines.

Over 40% renewable market share in 2025 is locked in – We can summarise the above the discussion in the following table:

Hands up if you think the NSW REZs will result in new projects being announced? Or the VRET 0.8 GW auction?

You don’t have to try very hard to see a further 5GW of new projects being announced over the next five years. There is over 3GW of capacity in the Orana/Central West REZ that the NSW state government has fully committed to getting going over the next couple of years and, of course, there was the 30GW expression of interest in bidding for that capacity.

As well as everything else the positive response to the NSW announcement means that the NSW government is likely to accelerate its second REZ development. After all, as Joh Bjelke Peterson was wont to say, “if the chooks cluck, feed them.” Dear old Joh.

Then there was the very strong expression of interest in the separate but adjacent Transgrid REZ proposal (Northern slopes and plains) corridor around Gunnedah/Tamworth.

Finally, in terms of State Government support there is the headline announcement of another 0.8GW of VRET in Victoria. That would be a further 13-14TWh and would eat another coal generator, say Eraring, which Kerrie Schott has stated needs a new coal ash dam.

What could possibly go wrong? – The downsides to the above estimates are:

Firstly, transmission may not be available to connect all the new generation. Most obviously Project Interconnect from South Australia to NSW is still sitting in the zombie land hands of the AER, having already been there for nine months. Yep, that’s progress on speeding up transmission development in Australia.

Secondly, there may end up being spilled wind and solar. Most modelling of the least-cost of an optimised system has some spilled solar and even wind. Mostly, though, the models don’t explain how the solar developer gets paid for the spilled output. No doubt a pat on the back and a quiet word that they’ve done their bit will suffice.

Thirdly, rooftop solar could slow down much more than shown in this note. Fourthly, there may be issues with inertia. The one area that I think the ESB, AEMC and AEMO need to think even harder about is building micro-grids into the existing main grids and distributing inertia, but those issues will at worst only slow down this new capacity.

Fifthly, some may say there is not enough dispatchable power, but at 50% wind and solar, and that includes 8-9% highly dispatchable, at least within Tasmania, hydro, we don’t see there is any issue with dispatchable power. Where one might imagine a problem is reliability, as the daily ramping requirement increases, but this will incentivise longer duration batteries (4 hours) which can easily smooth the ramp.

Sixthly, projects may proceed very slowly. The industry is more cautious now and there is less reason to rush as the LRET carrot is no longer dangling and power prices are less supportive.

As against that, if coal generators do close early, as looks increasingly likely to ITK, then that will of course lead to short term (2-3 year) higher prices and you’d like to have your facility on line for that. There is lots and lots more to say but that’s enough for one day.

“Morrison claims Gas needed because Batteries can’t yet Firm like Wind & Solar” Article in Renewable Economy, 29th September 2020 by Michael Mazengarb:

“Prime Minister Scott Morrison has again suggested that gas is the only technology available to firm supplies of wind and solar generation, saying that batteries have yet to be built at sufficient scale.

The comments came during an address to the National Press Club on Thursday ahead of the federal budget, announcing a new $1.3 billion ‘Modern Manufacturing Initiative’. They appear to contradict a range of expert analysis about the capabilities of battery technologies, including the Integrated System Plan prepared by AEMO as a blueprint for the future energy system.

Asked about the role of gas in the energy market, Morrison said that he was focused on the development of new gas resources, as he did not think battery storage would be in a position to deliver sufficient firming capacity.

“Gas is a way of supporting renewable investment, renewable energy sources. When you look at the per unit cost of electricity that comes from all the various sources, whether it’s solar, wind or gas or others, you need to compare it on a reliability measure,” Morrison told the National Press Club.

“And to make the record investment that we’ve had in renewables work better for the system, it needs the firming capacity. Now, we know that batteries are not at that scale yet. They’re not at that scale yet.”

“And gas is – as I said, it selects itself because there is not another resource that can so quickly peak to support the renewables,” Morrison added.

“Why Green Hydrogen could be Cheaper than Fossil Fuels in just a Few Years” Article Renew Energy, written by Micheal Mazengarb, 28th September 2020:

“New research suggests that bigger and better electrolysers will be key to producing green hydrogen at a lower cost than fossil fuels, and Australia’s abundance of cheap solar means this cross-over point will come ‘sooner rather than later’.

The analysis has been detailed in a paper published in in the journal Cell Reports Physical Science, which identifies the potential pathways for a renewable hydrogen to achieve cost competitiveness with fossil fuels, including gas, coal and transport fuels.

Researchers from the University of New South Wales modelled a number of technology scenarios to build an understanding of the cost drivers of renewable hydrogen and where there were opportunities to drive down costs.

The study found that the current cost of renewable hydrogen ranged between $AUD4.04 to $AUD6.53 per kilogram, but the researchers were able to identify scenarios that would deliver renewable hydrogen costs consistent with targets to get production costs below $2 per kilo, a widely recognised benchmark where renewable hydrogen becomes competitive with fossil fuels.

“After plugging all these different values into our algorithm and getting a range of prices of hydrogen energy, we then said, ‘Okay, so there were some cases where we got closer to that $US2 per kilogram figure ($AUD2.80). What was it about those cases that got it down so low?’” report co-author Nathan Chang said.

“Capital costs of electrolysers and their efficiencies still dictate the viability of renewable hydrogen,” co-author Dr Rahman Daiyan added. “One crucial way we could further decrease costs would be to use cheap transition metal-based catalysts in electrolysers. Not only are they cheaper, but they can even outperform catalysts currently in commercial use.”

“Studies like these will provide inspiration and targets for researchers working in catalyst development.”

The study found that reductions in the cost of electrolyser technologies will be the key to getting the cost of producing renewable hydrogen to a globally competitive level, and that is is likely that renewable hydrogen will soon be produced at a lower cost to that produced using fossil fuels.

In particular, the UNSW researchers found that Australia is well placed to lead the emergence of a commercially viable renewable hydrogen industry that can out compete fossil fuels, leveraging Australia’s abundance of solar resources.

The analysis found that it will be possible to produce low cost hydrogen in remote parts of Australia, where the solar resource could be maximised and would avoid the need to invest in new grid infrastructure.

Regions like Port Hedland in Western Australia could deliver competitively priced renewable hydrogen into export markets like Japan and South Korea, which are both aiming to boost their use of renewable hydrogen but do not enjoy the same access to solar resources as Australia does.

The research has been prepared with the support of the Australian Renewable Energy Agency (ARENA), which is preparing to provide $70 million in funding support for several large-scale electrolyser projects in Australia.

Low emissions hydrogen featured prominently in the Technology Roadmap recently unveiled by the Morrison government, but which will advocate for investment in fossil fuel hydrogen paired with carbon capture and storage alongside renewable hydrogen.

However, the researchers said that it was only a matter of time before renewable hydrogen became a cheaper source of energy than traditional fossil fuels, with the cost of solar energy continuing to fall dramatically.

“Because PV costs are reducing, it is changing the economics of solar hydrogen production,” Dr Chang said.

“In the past, the idea of a remote solar driven electrolysis system was considered to be far too expensive. But the gap is reducing every year, and in some locations there will be a cross-over point sooner rather than later.”

The researchers added that it was crucial that governments played an active role in helping to increase the scale of production, including by supporting the development of bigger and better electrolyser technologies.

“With technology improvements in electrolyser efficiency, an expectation of lower costs of installing these types of systems, and governments and industry being willing to invest in larger systems to take advantage of economies of scale, this green technology is getting closer to being competitive with alternative fossil fuel production of hydrogen,” Dr Daiyan added.

Disclaimer The comments and details in the articles in this newsletter do not reflect the views, policies or position of the Association or its member Councils and are sourced and reproduced from public media outlets by the Executive Officer to provide information for members that they may not already be exposed to in their Local Government areas

Contacts

Clr Peter Shinton (Chair) peter.shinton@warrumbungle.nsw.gov.au 0268492000 or Greg Lamont (Executive Officer) 0407937636, info@miningrelatedcouncils.asn.au.

You must be logged in to post a comment.